WASHINGTON, DC, June 9, 2023 (ENS) – Global economic growth has slowed, and the risk of financial stress in emerging market and developing economies, known as EMDEs, is intensifying, hemmed in by high global interest rates, according to the World Bank’s latest “Global Economic Prospects” report, issued Tuesday.

Global growth is projected to slacken from 3.1 percent in 2022 to 2.1 percent in 2023, the World Bank Group projects in the report, warning that low-income economies are in “dire straits.”

“The global economy is set to slow substantially in 2023. The lagged and current effects of monetary tightening, as well as more restrictive credit conditions, are expected to weigh on activity in the second half of the year, with weakness persisting into 2024, blogged World Bank economists Dominik Peschel and Phil Kenworthy, who contributed to the report.

“Tight monetary policy in the United States, in particular, can adversely affect EMDEs in several ways. It slows the U.S. economy, which reduces demand for EMDE exports, and tends to lead to higher interest rates in EMDEs,” Kenworthy wrote.

In EMDEs other than China, growth is set to slow to 2.9 percent this year from 4.1 percent last year. These forecasts reflect what the bank calls “broad-based downgrades.”

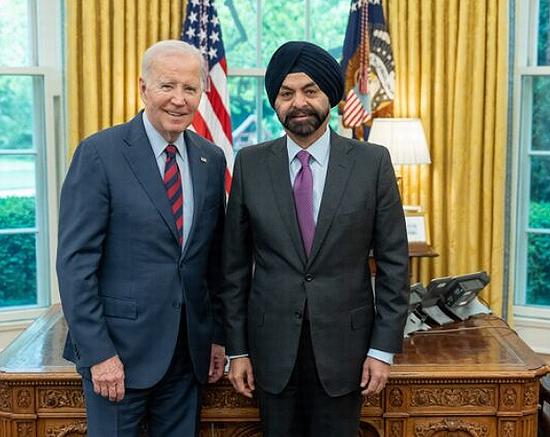

“The surest way to reduce poverty and spread prosperity is through employment – and slower growth makes job creation a lot harder,” said the World Bank Group’s new President Ajay Banga. “It’s important to keep in mind that growth forecasts are not destiny. We have an opportunity to turn the tide but it will take us all working together.”

Banga replaced Trump-appointed David Malpass as World Bank Group president on June 2. He is the first India-born American to hold the position. Banga comes to the job from leadership of the global growth equity investor General Atlantic.

Born in Pune, Maharashtra in 1959, Banga became a naturalized U.S. citizen in 2007. He began his career at Nestle in the early 80s and has served as a board member at multinational organizations including Citigroup, American Red Cross, Kraft Foods and Dow, Inc. He worked at Mastercard for over a decade, as president, chief executive, and executive chairman.

Banga was selected by President Joe Biden, who called him, “a transformative leader, bringing expertise, experience, and innovation to the position of World Bank President.”

“Together with World Bank leadership and shareholders, he will help steer the institution as it evolves and expands to address global challenges that directly affect its core mission of poverty reduction – including climate change. Ajay will also be integral in bringing together the public and private sectors, alongside philanthropies, to usher in the fundamental changes in development finance that this moment requires,” President Biden said.

“I look forward to working with Ajay in his new role and to supporting his efforts to transform the World Bank, which remains one of humanity’s most critical institutions to reduce poverty and expand prosperity around the globe,” the President said.

Banga is taking over the World Bank Group at a time when most EMDEs are “sailing in dangerous waters,” the report warns, although these emerging market and developing economies “have seen only limited harm from the recent banking stress in advanced economies so far.”

With increasingly restrictive global credit conditions, one out of every four EMDEs has effectively lost access to international bond markets, according to the report. The squeeze is especially acute for EMDEs with underlying vulnerabilities such as low creditworthiness. Growth projections for these economies for 2023 are less than half those from a year ago, making them highly vulnerable to additional shocks.

“The world economy is in a precarious position,” said Indermit Gill, the World Bank Group’s chief economist and senior vice president, and an Indian national. “Outside of East and South Asia, it is a long way from the dynamism needed to eliminate poverty, counter climate change, and replenish human capital.”

“In 2023, trade will grow at less than a third of its pace in the years before the pandemic,” Gill said. “In emerging markets and developing economies, debt pressures are growing due to higher interest rates. Fiscal weaknesses have already tipped many low-income countries into debt distress. Meanwhile, the financing needs to achieve the sustainable development goals are far greater than even the most optimistic projections of private investment.”

The latest forecasts indicate that the overlapping shocks of the pandemic, the Russian invasion of Ukraine, and the sharp slowdown amid tight global financial conditions have dealt an enduring setback to development in EMDEs, one that will persist for the foreseeable future.

By the end of 2024, economic activity in these economies is expected to be about five percent below levels projected on the eve of the pandemic.

In low-income countries – especially the poorest – the damage is stark: in more than one-third of these countries, per capita incomes in 2024 will still be below 2019 levels. This feeble pace of income growth is expected to entrench extreme poverty in many low-income countries.

“Many developing economies are struggling to cope with weak growth, persistently high inflation, and record debt levels. Yet new hazards – such as the possibility of more widespread spillovers from renewed financial stress in advanced economies – could make matters even worse for them,” said Ayhan Kose, deputy chief economist of the World Bank Group, and a Turkish national.

“Policy makers in these economies should act promptly to prevent financial contagion and reduce near-term domestic vulnerabilities,” Kose said.

In advanced economies, growth is set to decelerate from 2.6 percent in 2022 to 0.7 percent this year and remain weak in 2024, the report says.

After growing 1.1 percent in 2023, the U.S. economy is set to decelerate to 0.8 percent in 2024, mainly because of the lingering impact of the sharp rise in interest rates over the past year and a half.

In the euro area, growth is forecast to slow to 0.4 percent in 2023 from 3.5 percent in 2022, due to the lagged effect of monetary policy tightening and energy-price increases.

The report offers an analysis of how increases in U.S. interest rates are affecting emerging market and developing economies. Most of the rise in two-year Treasury yields over the past year and a half has been driven by investor expectations of hawkish U.S. monetary policy to control inflation.

According to the report, this particular type of interest rate increases is associated with adverse financial effects in EMDEs, including a higher probability of financial crisis. These effects are more pronounced in countries with greater economic vulnerabilities.

In particular, frontier markets – those with less developed financial markets and more limited access to international capital – tend to see outsized increases in borrowing costs. For instance, sovereign risk spreads in frontier markets tend to rise by more than three times as much as those in other EMDEs.

In addition, the report provides a comprehensive assessment of the fiscal policy challenges confronting low-income economies. These countries are in dire straits. Rising interest rates have compounded the deterioration in their fiscal positions over the past decade. Public debt now averages about 70 percent of GDP. Interest payments are eating up a rising share of limited government revenues. 14 low-income countries are already in, or at high risk of, debt distress.

Spending pressures have risen in these low-income economies. Adverse shocks such as extreme climate events and conflict are more likely to tip households into distress in low-income countries than anywhere else because of limited social safety nets. On average, these countries spend just three percent of GDP on their most vulnerable citizens – well below the 26 percent average for developing economies.

Download the full report: https://bit.ly/GEPJune2023FullEN

Download growth data: https://bit.ly/GEPJune2023Data

Download charts: https://bit.ly/GEPJune2023AllCharts

Regional Outlooks:

East Asia and Pacific: Growth is expected to increase to 5.5 percent in 2023 and then slow to 4.6 percent in 2024. For more, see regional overview.

Europe and Central Asia: Growth is expected to edge up slightly to 1.4 percent in 2023 before increasing to 2.7 percent in 2024. For more, see regional overview.

Latin America and the Caribbean: Growth is projected to slow to 1.5 percent in 2023 before recovering to 2 percent in 2024. For more, see regional overview.

Middle East and North Africa: Growth is expected to slow to 2.2 percent in 2023 before rebounding to 3.3 percent in 2024. For more, see regional overview.

South Asia: Growth is projected to edge down to 5.9 percent in 2023 and then to 5.1 percent in 2024. For more, see regional overview.

Sub-Saharan Africa: Growth is expected to slow to 3.2 percent in 2023 and rise to 3.9 percent in 2024. For more, see regional overview.

Featured image:

© 2023, Environment News Service. All rights reserved. Content may be quoted only with proper attribution and a direct link to the original article. Full reproduction is prohibited.